Imagine paying for insurance that might never give you back a single rupee. Shocking, right? Welcome to the less-discussed world of life insurance in India.

In the midst of economic uncertainty, understanding the difference between Term and Whole Life insurance has become vital. This one decision could alter your financial security forever.

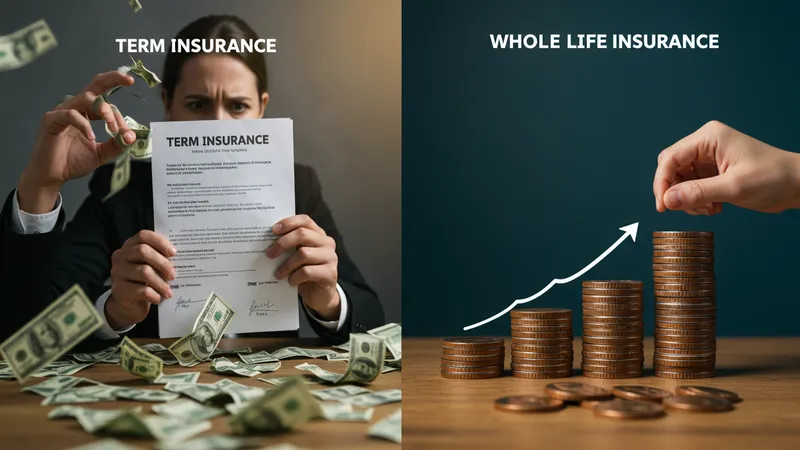

Most people believe that insurance is a waste of funds unless you’re retiring. But did you know that term insurance doesn't pay you back anything if you outlive the policy? That's right; it's like betting against yourself! Many choose term insurance for its lower premiums, unaware that once the term ends, there’s nothing left to gain. But that’s not even the wildest part…

Whole Life Insurance, on the other hand, offers peace of mind and an investment. With its lifelong coverage and ability to accumulate cash value, it seems like the ultimate choice. However, the higher premiums make it less accessible for the average earner. Even so, this seems like a smart move for those who can afford it. But again, what you’re not told about this might leave you stunned…

Despite knowing these differences, choosing the best option isn't straightforward. The misconceptions surrounding life insurance can drain your wallet or worse, leave you unprotected. As experts debate over the better option, what happens next shocked even the experts...

Let's delve into the real cost of term insurance. While the upfront premium might seem budget-friendly, it often comes with hidden penalties. Miss a single payment, and your entire plan might get nullified. You won’t just lose coverage; you might end up paying double to restart a new plan. This hidden pitfall isn't something agents proudly highlight, often leaving consumers in the lurch. But there's one more twist that will make you rethink the term insurance as a cost-effective option...

Whole Life Insurance, with its high costs, sounds daunting, doesn't it? Interestingly, it includes a savings component that builds over time. This means you’re not just paying for a safety net. However, it’s essential to realize those savings don't always stack up as quickly as you might hope. Unforeseen charges and fluctuating interest rates could slow the growth, making it less beneficial than it sounds. What you read next might change how you see whole life policies forever.

The term versus whole life insurance debate centers around uncertainty. Both are riddled with perplexing fine print, and since many Indian policies follow unique regulations, the complexity escalates. Without a specialized advisor, navigating these waters can seem impossible. But there’s one insider tip that might simplify your decision...

For many Indians, cultural norms gravitate towards long-term security, often leaning towards whole life insurance. Despite higher premiums, people bank on lifelong coverage due to the persistent uncertainty. Yet, an emerging trend is shifting perspectives, with an unexpected insurance strategy capturing attention. Stay tuned for this game-changer that could revolutionize your approach to coverage...

Riders are insurance add-ons that can transform a basic policy into an extraordinary one. But how many are familiar with them? Consider this: a critical illness rider could offer a financial backup during a health crisis, and still, it remains an overlooked option in term life plans. This ignorance often costs families dearly when the primary insured faces unforeseen health issues. However, this is just the beginning of how riders can change your policy landscape...

Whole Life Insurance policies can include riders for more than just illnesses. Do you know you could add an accidental death benefit or a family income benefit rider? These enhancements could significantly improve policy efficiency. An accidental death rider might pay double if death occurs in an accident, providing additional security to the beneficiary. Yet, the thought of higher premiums often deters buyers. But what if there’s a way to maximize protection without breaking the bank?

Most policyholders focus narrowly on the primary benefits, missing out on these potentially life-altering enhancements. A disability waiver of premium rider, for instance, could maintain your policy's active status even if you can no longer work. It is opportunities like these that can define the difference between surviving and thriving. And just when you think you've heard it all, the optimal combination to ensure maximum security is still to come...

Recently, an emerging trend involves the introduction of more flexible, customizable rider options within life insurance policies. Far from redundant add-ons, these are now tailored to cater to different age groups and lifestyles. Understanding which riders best fit your circumstances is crucial: it is the key to turning your basic plan into something that feels tailor-made, even luxurious. But what no one tells you is how the real optimization happens not in the product, but in your choices...

Insurance companies aren’t just selling policies; they’re selling peace of mind. But have you considered how psychological triggers influence your choice of policy? Let's contemplate the fear of missing out — FOMO — often exploited to push term insurance's low premiums. The assurance of financial safety draws many, without contemplating the absence of maturity benefits, sparking a false sense of security. But wait, there's more to this psychological maneuvering...

Whole Life Insurance takes this play a step further, leveraging the Indian penchant for long-term security and legacy planning. The psychological comfort of leaving something tangible for future generations often outweighs the immediate high cost of premiums. Still, does this long-term peace genuinely justify the higher financial outlay? The more you probe, the more you find layers to this equation worth unraveling...

A crucial point often overlooked is the emotional impact of insurance decisions on family dynamics. Whole Life Insurance is often seen as a multigenerational asset, fostering goodwill among heirs. However, the emotional burden it places on policyholders during their lifetime isn't always accounted for. Overcome by guilt and obligation, some individuals compromise on present opportunities to ensure their family's future security. But what if there's more than meets the eye in this emotional balancing act?

New psychological studies suggest that the peace-of-mind factor offered by whole life policies does not always correlate with happiness. Instead, a strategic mix of insurance types tailored to individual financial goals often yields better satisfaction. This personalization stands in stark contrast to the one-size-fits-all sells, suggesting a new frontier in insurance planning. Could this innovative intersection between psychology and finance redefine how we protect our futures? The next revelation might just astonish you...

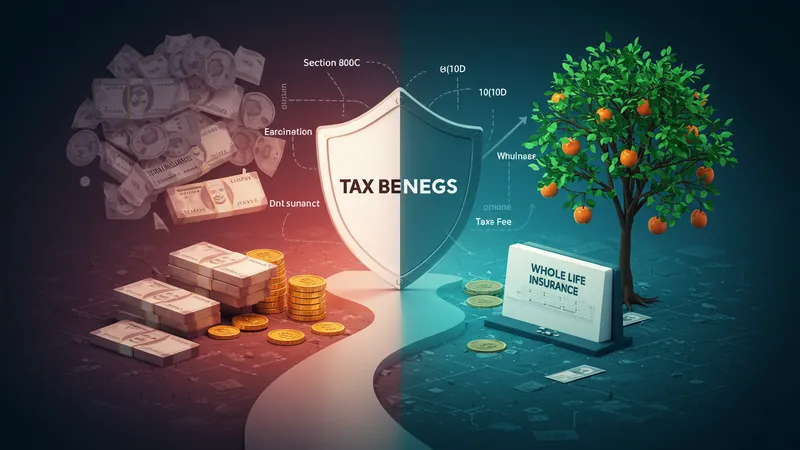

Imagine harnessing the tax benefits of insurance in such a way that it boosts not just savings but enhances your financial lifestyle. Both term and whole life insurance present opportunities under Section 80C and 10(10D) of the Income Tax Act. However, many policyholders are unaware of how to maximize these benefits. Here's the catch: leveraging these tax incentives effectively changes the play from mere savings to strategic investment. But you haven’t heard it all yet...

While both policies offer tax deductions, understanding their nuances can amplify returns. Term insurance premiums up to ₹1.5 lakh are exceptionally alluring for individuals seeking deductions. Contrast this with the potential for entire life insurance policies, where maturity proceeds can be tax-free if criteria are met. What's often understated is how these policies can serve as lucrative tax shields. Yet there’s more waiting to surprise you...

Notably, whole life insurance premiums may be more considerable, but they often sit outside conventional investment limits, leading to better portability for tax exemption prospects. There's a strategy to blend term policy tax benefits with long-term whole life gains that goes beyond basic savings, leaning into wealth accumulation. As the tax landscape shifts, this synergy could redefine traditional financial planning. And yet, there’s another hidden layer to consider, one not commonly discussed...

Increasing numbers of planners are delving into insurance as a tax optimization tool, combining its benefits with other fiscal instruments. This concoction can shape a fiscally rewarding strategy that aligns with life goals, optimizing wealth beyond tax savings alone. As this perspective gains traction, the melding of insurance and tax planning becomes not just prudent, but innovative. Could this blended approach be the answer to mastering financial growth while maintaining secure insurance coverage? The conclusions might challenge everything you thought you knew...

The landscape of insurance in India is on the cusp of transformative change. Technological advancements like AI and machine learning are reshaping how policies are crafted, evaluated, and purchased. Imagine AI-driven insights guiding your policy enhancements or monitoring critical variables affecting your premiums in real-time. These advancements aren’t just futuristic—they’re happening now, yet only a fraction fully apprehend their potential. But that’s just the tip of the iceberg...

The era of one-size-fits-all insurance is phasing out as customizable, data-driven policies take precedence. The integration of blockchain technology promises unprecedented transparency and verification efficiency. Such innovations mean that customers will now tailor policies that fit their unique situations with pinpoint accuracy. This personal touch is set to redefine satisfaction and reliability within the industry. Want to peek deeper into this evolving sphere?

Regulatory changes are also poised to impact insurance as we know it. New norms that prioritize consumer benefits over corporate profit are emerging. This shift ensures competitive pricing and enriched consumer protection mechanisms. But, as always, there’s a catch: are these regulatory shifts reactive measures, or could they lead to innovative consumer-oriented products? Only time will unveil the extent to which regulations will shape the future of insurance...

Consider the looming influence of digital platforms dominating the Indian insurance market. As more purchasing moves online, the way people evaluate terms vs. whole life policies continues to morph dramatically. Faster processing, real-time advice, and instant comparisons now define decision-making landscapes. Are we moving towards unprecedented convenience in decision making, or is this ease masking deeper complexities yet unravelled? Stay tuned as we explore this closely, and what comes next might ultimately reshape your perspective...

Insurance and millennials—what a combination! Unlike their predecessors, millennials are more informed, questioning, and digitized in approach. They lean towards policies that align with their fast-paced lifestyles, usually favoring term over whole life plans. But here lies a contradiction: millennials' health-oriented choices might suggest a shift towards comprehensive coverage instead. It’s a fine line between frugality and future preparedness, an eternal struggle with a modern twist...

Interestingly, awareness of insurance insufficiencies runs high among millennials. Practicality often surpasses brand loyalty, as these young adults seek flexible policies offering maximum bang for their buck. Customizable plans meeting specific needs are the go-to, overshadowing traditional fixed-term avenues. Ironically, the seeming avoidance of whole life policies may point to yet another emerging trend: investment in more diverse portfolios. But what’s the hidden twist in this evolving scenario?

What stands out is the proactive financial education amongst millennials; they’re intent on financial literacy, attending seminars, and engaging with peer advice. It's a do-it-yourself approach that questions archaic insurance norms. Yet, as they foster informed decision-making, one major paradox remains: the increasing allure of instant gratification in the face of necessary long-term planning. Could there be more at play beneath the surface than this apparent contradiction?

The growing emphasis is on balancing indulgence and responsibility, where unique financial products are sought to bridge the gap. Digitalized advisors are stepping into this space with tailored offerings that blend flexibility and foresight. As you ponder these elements, consider how evolving millennial needs could redefine traditional life insurance approaches, catapulting the industry into uncharted territories. Brace yourself, for the continuation of this narrative offers insights guaranteed to rival even your wildest anticipations...

Did you realize that a stark gender disparity exists within the insurance landscape in India? Women remain underrepresented and underrated within policy acquisition. Though societal norms evolve, this is an area where substantial progress is yet required. But what’s the unseen catalyst behind this gap, and why does it matter so much?

The lower insurance cover among women stems from deeply entrenched norms regarding financial dependency. While the increase in working women is well-documented, insurance statistics remain incongruent with such advancements. Millennials indeed offer a glimmer of hope, yet persisting institutional biases necessitate more than a superficial glance. What pivotal measures will truly alter these ingrained perceptions?

A significant but often overlooked factor contributing to gender skew is the undervaluation of women's roles, particularly in rural India. Protecting female-laden roles associated with home and family could grant equilibrium not only in protection but in economic valuation of domestic roles. Marrying this underappreciated potential with cultivating community education initiatives might redefine female economic inclusion.

Empowering women through targeted insurance efforts is essential—imagine targeted policies and campaigns specifically designed for and marketed to women. Envision the pioneering entities focusing their efforts on bridging this divide. It’s an invitation to challenge assumptions and embrace transformative inclusivity. What eventual ramifications might these efforts unleash for gender parity in insurance, and beyond? This narrative propels us forward, promising revelations that might just surprise you...

Understanding when to surrender a policy can be a bewildering endeavor. Unveiling the complexities of policy surrender charges for whole life insurance, many policyholders overlook these nuances and end up paying much more than anticipated. Yet, a strategic surrender could potentially recuperate part of your investment. The insight is vital yet under-discussed—is there a hidden strategy to policy surrender?

An often-misjudged element is the mortality charge—part of the insurance premium that supplies a death benefit. Are you aware of how it fluctuates with age? Increasing annually, these charges escalate your premium, slowly eroding savings potential within your policy's cash value. Peering into these nuances can present unexpected savings or loss prevention. Comprehending these factors isn't just insightful; it's imperative. But there's more to unfolding these keys...

Evaluation and strategic planning of mortality charges within whole life policies could determine long-term financial clarity. Addressing potential pitfalls ahead of time bolsters present and future monetary security. Learn to manipulate these figures adeptly, and they offer a strategic advantage, yet often remain hidden behind more marketed policy features...

A comprehensive understanding requires exploring how maneuvering through these charges ultimately affects policy resale value. Your choice—surrendering, maintaining, or transferring a policy—determines your financial road map. This avenue of insurance strategy not only empowers but educates policyholders, redefining control over financial planning long after the policy was purchased. Contemplate this as we delve into consequential findings, insights poised to transform financial clarity...

Did you ever consider that climate change might reshape life insurance as we know it? The environmental dogma doesn't merely affect physical conditions but reverberates through life calculation metrics. The integration of risk factors, including life expectancy connected with environmental variances, is emerging. But how does this impact your insurance decisions?

Climate change implications are extending to health, thus affecting risk assessments within policy calculations. More unpredictable weather and health-related contingencies could shift insurance premiums and terms. Astute consumers may now evaluate the impact of environment-derived statistics on their policies. It uncovers an intersectional yet unexplored viewpoint. Yet there’s a direction to this evolution...

Industries are gradually inclining toward ecological consideration in policies, factoring in eco risks into overall policy pricing and conditions. Such movements echo a wider understanding of life conditions beyond mere actuarial calculations. Enter the next advisory concept: green policies and environmentally indexed premiums may delineate how to face forthcoming realities. This burgeoning sector not only resonates with lifestyle but propels thought-forward planning toward a sustainable future...

If you believed life insurance's future lay solely in consumer behavior and economic shifts, reevaluate this standpoint. The inexorable impact of global ecological concerns poses radical avenues, both risky and insightful. Insurance evaluation must now include forthcoming eco-realities, underscoring preparedness for a future not only economically sustained but ecologically resilient. Consider these shifts as we discuss ensuing paradigms, promising foresight into potential realignments within policy infrastructure...

Cultural mores and life insurance in India present an intricate tapestry affected by tradition, collective values, and evolving aspirations. Remember how every milestone—marriages, children, and retirement—binds financial responsibilities to roots? This cultural reflection is ingrained in India’s insurance psyche. Yet beyond traditions lies a shifting cultural paradigm charting future scenes...

Cultural financial habits directly shape insurance inclinations. Many adopt insurance as ancillary to investments rather than standalone security, often modeling after family or community norms. But with education’s rising tide introducing holistic financial literacy, Indian households evolve into more independent units, nurturing self-designed financial blueprints. How might this cultural blend of evolution move forward?

The millennial emergence deeply influences insurance dynamics, beckoning recalibrations to meet contemporary cultural needs. Integrating distinctly Indian perspectives with global ideas presents a fusion—a tapestry entwining modernity with heritage. Emerging are insurance products encapsulating a collective mentality yet spotlighting individualistic aspirations. This intertwining cultural discourse might refine and redefine future insurance expectations...

Continual narrative-driven cultural shifts ordain not linear, but integrative changes, especially within insurance. Customization to meet these cultural trends arises, delivered through the transformation of products and policies to accommodate lifestyle fusion. As we navigate these cultural-infused lenses, delve deeper to unveil where these dynamics propel insurance, and how they might challenge preconceived notions of safety...

As we unveiled the intricate differences, hidden truths, and surprising angles surrounding term and whole life insurance in India, it's evident these choices aren't just financial but deeply personal, cultural, and future-driven decisions. Whether pondering cost, emotional weight, or emerging trends, the landscape is constantly evolving, urging you to empower your choices with knowledge.

Which of these revelations sparked a shift in your perspective? If you found insight or intrigue within these pages, share this journey with others. Bookmark this article as a reference for strategizing your insurance decisions, securing not only futures but peace of mind. Equip yourself with understanding, for today’s insights are tomorrow's actions.